When you sign up for an open banking app that pulls your transaction history from your bank, you’re not just sharing data with that app. You’re giving it permission to pass your information to advertisers, credit checkers, budgeting tools, and dozens of other services you’ve never heard of. Most people don’t realize this. And if you’ve ever clicked "Accept All" on a cookie banner and later found your data showing up in targeted ads you didn’t sign up for, you’ve felt the fallout of poor consent management.

What Consent Management Really Means for Open Banking

Consent management in open banking isn’t just a checkbox. It’s the system that decides who gets your financial data, when, and under what rules. Under regulations like GDPR and the California Privacy Rights Act (CPRA), financial institutions and fintech apps must get your explicit, specific, and revocable permission before sharing your data with third parties. That means if you allow an app to access your spending habits to build a budget, you should also be able to say no when that same app wants to sell your data to a credit scoring company or an insurance provider.

Without proper consent management, open banking becomes a data pipeline - and you’re the product. A 2023 study by the Norwegian Consumer Council found that 41% of websites claiming to honor user consent still sent data to third parties after users said no. In open banking, where financial data is sensitive and highly valuable, this isn’t just a privacy issue - it’s a compliance risk that can trigger fines up to 4% of global revenue under GDPR.

How Third-Party Access Works - And Why It’s So Hard to Control

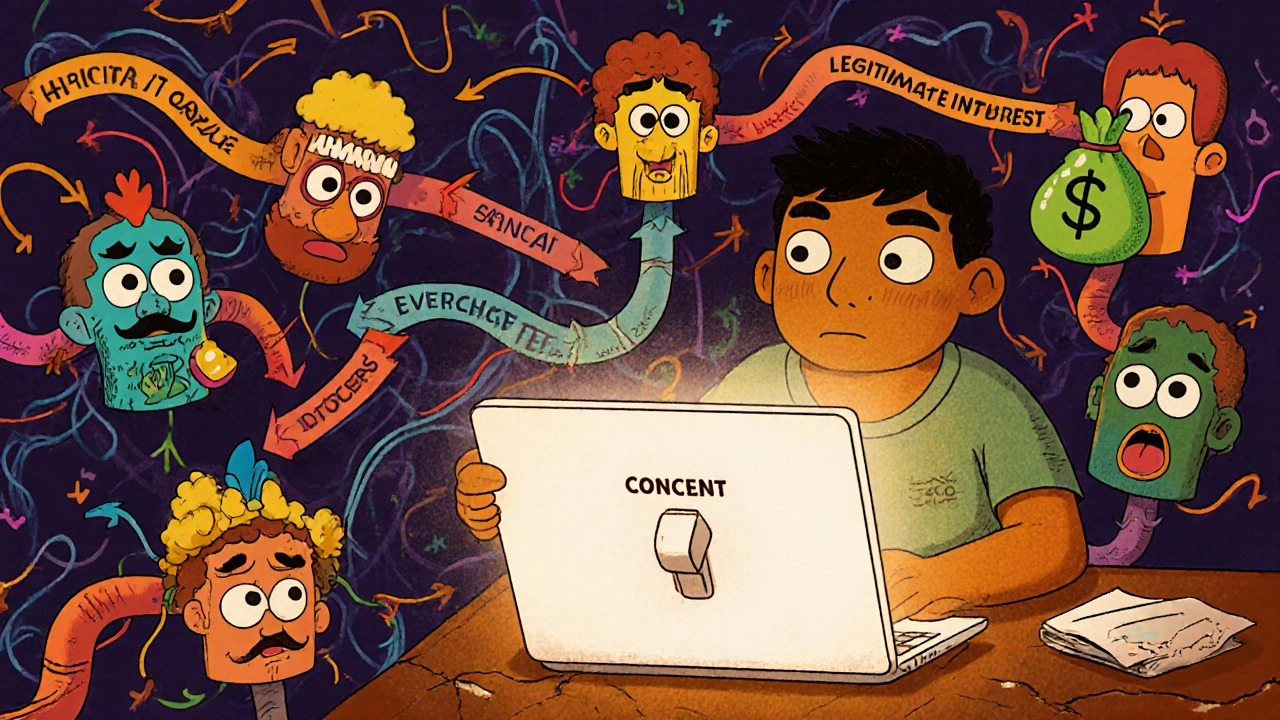

When you connect your bank account to a finance app, the app doesn’t directly pull your data. It uses APIs provided by your bank, which then route your information through a chain of services: analytics tools, fraud detectors, identity verification providers, advertising networks, and data brokers. Each of these is a third party.

Here’s the problem: most consent tools only let you choose between "Accept All" or "Reject All." But that’s not how real data sharing works. You might be fine with a budgeting tool accessing your income data but not want your spending habits shared with a marketing firm. Granular consent means being able to toggle permissions for each third party individually - like a switchboard where you decide who gets access to what.

Leading platforms like OneTrust and Usercentrics offer this level of control. They let users see a list of every company that will receive their data, with explanations like: "This company uses your transaction history to show you personalized loan offers." But implementation is messy. Many apps still bundle third parties under vague labels like "Analytics Partners" or "Marketing Services," making it impossible for users to make informed choices.

The Technical Side: How Consent Is Enforced (or Not)

Behind the scenes, consent management relies on JavaScript-based systems that block or allow third-party scripts in real time. When you deny consent for Facebook Pixel, the system should prevent Facebook’s tracking code from loading. If it doesn’t, your data still flows - even if the banner says you said no.

Modern Consent Management Platforms (CMPs) integrate with tools like Google Tag Manager and customer data platforms (CDPs) to ensure preferences are honored everywhere. If your CRM system or email provider isn’t synced with the consent system, data leaks happen. A marketing director at a Fortune 500 company reported that after fixing these gaps, their customer trust scores jumped 23% - without losing data quality.

But many systems still fail. The International Association of Privacy Professionals (IAPP) found that 68% of companies take 3 to 6 months to properly configure third-party vendor lists. Why? Because companies often don’t even know who all their data partners are. One enterprise found 47 third parties accessing customer data - and half of them weren’t listed in any contract.

Regulations Are Catching Up - But Not Fast Enough

GDPR, which took effect in 2018, was the first major law to demand specific consent for third-party data sharing. It requires that consent be "freely given, specific, informed, and unambiguous." That means pre-ticked boxes? Illegal. Bundled consent? Illegal. Vague descriptions? Illegal.

The CPRA, which came into force in January 2023, added another layer: for sensitive financial data, companies must now get opt-in consent - not just opt-out. That’s a big deal. It means if you want to share your bank balance with a loan app, you have to actively say yes. You can’t just ignore a pop-up and hope for the best.

Even the European Data Protection Board (EDPB) stepped in with guidance in late 2022, warning that "silos" of consent - where different departments or apps collect separate consents for the same third party - violate the law. If your bank’s app asks for consent, and your insurance partner asks again for the same data, that’s not compliance. That’s confusion.

What’s Broken - And What’s Working

Here’s what users are saying:

- "I denied consent to 15 trackers on a single site - but my data still went to Facebook Pixel." - Reddit user, June 2023

- "I spend 20 minutes every time I use a new finance app just trying to figure out who gets my data. I give up and click Accept All." - Survey respondent, 2023

These aren’t edge cases. They’re the norm. Consent fatigue is real. People are tired of endless banners. But the alternative - giving up control - is worse.

On the flip side, some companies are getting it right. A UK-based neobank redesigned its consent flow to show users a simple list: "These are the companies that will see your data. You can turn each one on or off." They added icons and plain-language descriptions. User opt-in rates for essential services stayed above 85%, while unwanted data sharing dropped by 72%.

What worked? Transparency. Simplicity. Control.

The Future: Standardized Consent and the End of Third-Party Cookies

The tech world is shifting. Google’s Privacy Sandbox is phasing out third-party cookies by 2024. The W3C is developing new standards like the Conversion Measurement API to replace them with privacy-first alternatives. Meanwhile, IAB Europe updated its Transparency & Consent Framework (TCF v2.2) to force clearer disclosures about third-party data use.

But here’s the catch: replacing cookies doesn’t fix consent. It just changes the mechanism. The real challenge remains: how do you let users control who gets their data - without overwhelming them?

By 2025, Gartner predicts 60% of large enterprises will use centralized consent hubs - single systems that manage permissions across all apps, services, and third parties. That’s up from just 22% in 2022. The goal? One consent decision, honored everywhere.

Open banking will only thrive if users trust it. And trust doesn’t come from fancy tech or legal disclaimers. It comes from knowing exactly who has your data - and being able to take it back with one click.

What You Can Do Right Now

If you’re a consumer using open banking apps:

- Never click "Accept All." Look for a "Manage Preferences" option.

- Check what third parties are listed. If you don’t recognize them, search their name online - many are data brokers.

- Revisit your consent settings every few months. Third parties change their practices often.

- If you’re unsure, revoke access to apps you don’t actively use.

If you’re a business offering open banking services:

- Map every third party that touches your users’ data - even the ones you think are "just analytics."

- Use a CMP that allows granular, real-time blocking - not just cookie banners.

- Test your system: deny consent and use browser tools to see if third-party scripts still load.

- Document every data-sharing relationship. GDPR requires it - and so do your customers.

Consent isn’t a compliance box to check. It’s the foundation of trust in open banking. Get it right, and users will stay. Get it wrong, and they’ll walk away - and take their data with them.

What’s the difference between consent management and a cookie banner?

A cookie banner is just the pop-up you see. Consent management is the entire system behind it - the technology that blocks third-party trackers, stores your preferences, and ensures those choices are honored across every app and service. Many cookie banners don’t actually block anything - they’re just legal disclaimers. True consent management enforces your choices technically, not just visually.

Can I revoke consent after I’ve given it?

Yes - and the law requires it. Under GDPR and CPRA, users must be able to withdraw consent as easily as they gave it. That means apps must provide a clear, one-click way to revoke access to third parties. If you can’t find a "Manage Consent" option in the app settings, it’s likely not compliant.

Why do some finance apps still share my data even after I said no?

There are two main reasons. First, the consent system might be poorly implemented - scripts may still load even after you opt out. Second, some third parties use "legitimate interest" as a legal loophole to bypass consent. But under GDPR, financial data can’t be shared under legitimate interest unless it’s essential for the service you signed up for. If you’re not using a credit check tool, your spending data shouldn’t be going to a marketing firm.

Are open banking apps safer than traditional banks?

Not inherently. Traditional banks have stricter internal controls, but they’re also more likely to share data with third parties behind the scenes. Open banking apps give you more visibility into who gets your data - if they implement consent properly. The risk isn’t the app itself - it’s whether they manage third-party access responsibly. Choose apps that show you exactly who sees your data and let you turn it off.

What happens if I don’t give consent for third-party access?

You should still be able to use the core function of the app - like tracking your spending or creating a budget. If an app locks you out of basic features unless you allow all third-party data sharing, it’s violating GDPR and CPRA. Legally, they can’t make consent a condition of service unless the data sharing is essential to the service you’re signing up for.

Graeme C

November 17, 2025 AT 10:02Let me tell you, I clicked 'Reject All' on a finance app last week - thought I was safe. Two days later, my LinkedIn ads were showing me personal loan offers based on my coffee spending. Turns out, the CMP was just a decorative banner. No blocking. No enforcement. Just legal theater. GDPR says consent must be 'specific and informed' - but if the tech doesn't enforce it, it's just a joke wrapped in a compliance checklist. We need real technical controls, not pretty UIs that lie.

And don't get me started on 'Analytics Partners' - that’s corporate code for 'we sold your data to 17 shadowy brokers who don’t even have a website.' I’ve started screenshotting the third-party lists and posting them on Twitter. Someone’s gotta call this out.

OneTrust? Half their clients still leak data because they don’t audit their vendor lists. It’s not a tech problem - it’s a willful negligence problem. Companies know. They just don’t care until the fine hits.

I’m not anti-innovation. I’m pro-ownership. My bank account isn’t a data farm. Stop treating me like a walking API key.

Astha Mishra

November 19, 2025 AT 09:32It is truly a profound irony, is it not, that in an age where we are more connected than ever - where our financial lives are digitized, quantified, and commodified with algorithmic precision - we are simultaneously being asked to surrender our autonomy through interfaces designed to confuse, overwhelm, and ultimately, exhaust us?

I have spent hours, yes, hours, poring over consent banners that list 40+ third parties under labels like 'Marketing Ecosystem' or 'Performance Partners.' What does that even mean? Who are these entities? Are they registered? Do they have a privacy policy? Can I find them on Companies House? Most cannot.

And yet, the law says we must give 'informed' consent. But how can one be informed when the information is deliberately obfuscated? When the language is legalese disguised as simplicity? When the toggle switches are buried beneath five layers of dropdown menus?

Perhaps the real issue is not consent management - but consent literacy. We need public education campaigns, not just technical fixes. We need schools teaching digital autonomy as a fundamental right, like reading or arithmetic. We need regulators who punish not just the breach, but the design of the deception.

And if you think this is only about finance - think again. This is the blueprint for how all personal data will be harvested in the coming decade. If we fail here, we fail everywhere.

I do not wish to be a product. I wish to be a person. And I am tired of being treated like a dataset with a pulse.

Kenny McMiller

November 20, 2025 AT 02:38Look, the whole consent thing is just a band-aid on a hemorrhage. Third-party cookies are dying, sure - but now we’ve got fingerprinting, device IDs, probabilistic matching, and server-side tracking. The consent banners? Pure theater. You click 'Reject All' and the same trackers still fire via the backend via first-party proxies. It’s not even clever - it’s lazy.

And don’t get me started on 'granular consent.' Who the hell has time to toggle 50 switches for every app? That’s not empowerment - that’s UX terrorism. People don’t want control. They want trust. Build a system that’s secure by default and opt-in only for the essentials. Let users choose between 'Essentials Only' or 'Full Access' - no need to micro-manage every data broker.

Also, 68% of companies take 3–6 months to map vendors? That’s not a tech problem - that’s a management failure. If you don’t know who your vendors are, you shouldn’t be in fintech. Period.

GDPR’s great, but it’s like putting a lock on a door that’s already been kicked in. We need architectural change, not compliance checkboxes.

Dave McPherson

November 20, 2025 AT 04:38